Aliko Dangote's Sugar company has nearly quadrupled in price this year.

Last month, he announced a merger between his three Agro-Allied businesses, and each listed entity's price doubled in the month since the announcement. Studying what will probably be the most significant corporate action of 2023 and investors' reactions to it will yield important lessons for anyone curious about the Nigerian equities market, M&A deals, or the games that billionaires play.

As an investor over the last six years, I have seen how corporate actions have been an important catalyst for value realization. Considering that the complete terms of the deal haven't been disclosed to the market, it's possible that investors have been too busy making money to weigh the full financial implications of their positions. I searched for clues in each company's financial statements to find out what the market could be pricing in - and to answer three main questions I'd want to know as a shareholder:

Why is Aliko Dangote merging his companies?

Why is the market reacting so positively to the announcement?

How attractive are the offer terms to each involved party?

Thanks for reading Markets Markets Markets! Subscribe for free to receive new posts and support my work.

Merger Rationale

There's a lot of speculation that Aliko Dangote is merging his companies to bolster his position as the wealthiest man in Africa on the Forbes Billionaires list and to one-up his long-term rival, Abdulsamad Rabiu.

Mergers, however, are time-consuming projects that involve exorbitant fees to corporate lawyers and investment bankers and should only be undertaken with good reasons. But there is evidence that suggests that Forbes magazine and his petty rivalry could have played a role:

The announcement comes after a 30% loss in Aliko's net worth due to the devaluation of the naira.

The merger will put Dangote Foods in a similar position to BUA Foods regarding revenues and outstanding shares.

Nigerian billionaires are fond of holding 80%+ of the shares outstanding in their companies to keep prices high.

While this makes for exciting market gossip, this merger is likely happening simply because there is a financial incentive to do so.

Higher share prices mean that Dangote can access more money through credit facilities based on the value of his businesses. If combining three of his companies can increase their total value, he stands to benefit from a higher net worth and more options for managing liquidity - a vital concern after he sunk billions of dollars into his petroleum refinery.

BUA Foods plays an essential role in achieving this, but it has little to do with their perceived rivalry.

They are creating an entity that matches BUA Foods in financial metrics because Abdulsamad's food company trades at an average 16.8x earnings multiple. Prior to the recent appreciation, Dangote Sugar and NASCON had historical average earnings multiples around 7x and 11.2x, respectively. The idea is that the market will value a combined Dangote Foods similarly to BUA Foods.

These businesses had been severely undervalued for a long time, leaving enormous amounts of value to be unlocked.

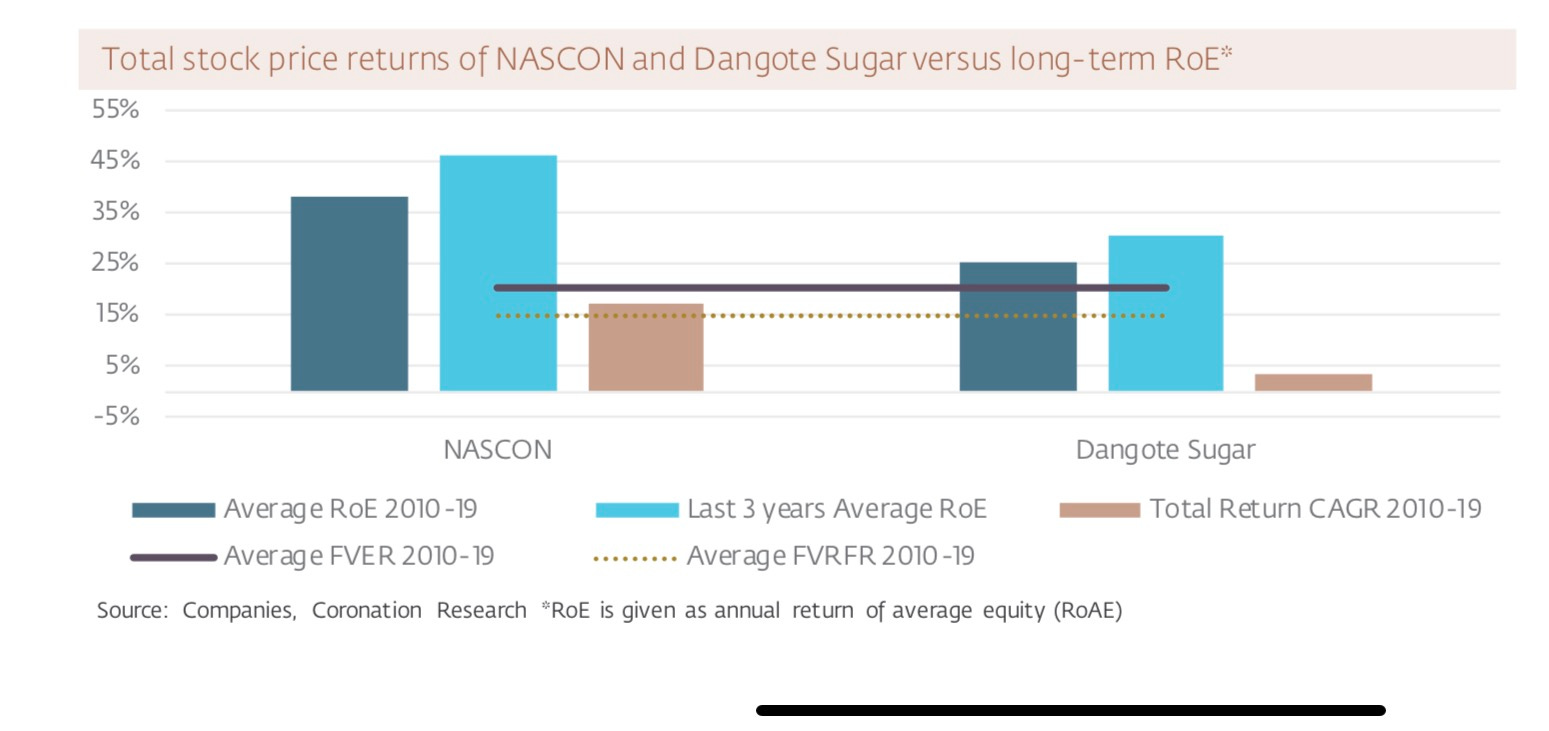

Within the Dangote group of companies are two specialized food producers, NASCON and Dangote Sugar, that have not only produced RoEs well in excess of our target of 20.53% but that have actually improved their RoEs in recent years. The result, unfortunately, has been total shareholder returns below our benchmark return. This is a case of unjust treatment by the market, quite likely a case of investors not paying attention to fairly small and not-very-liquid stocks.

I like this excerpt because it shows how the market can be wrong for over a decade and explains an inefficiency that will always exist in securities markets that savvy value investors can exploit.

How institutional investors operate is a significant determinant of securities prices, and the nature of their operations can create inefficiencies in places that are too small for them to pay attention to.

A merger of Dangote's three companies would create an entity large enough for institutions to invest in and research analysts to justify writing about - two factors that will likely lead to further expansion in multiples.

On the actual business side of things, some potential synergies may arise from combining the companies. However, it is hard to know what they are or what their magnitude will be until the explanatory statements by the financial advisers are published. In any case, most evidence points to this being primarily a multiples expansion play rather than a synergetic one.

Understanding The Transaction Structure

The transaction is set up as an internal restructuring to be executed through a scheme of merger.

The three businesses will be combined with Dangote Sugar Refinery as the surviving entity. The expectation is that the new company will be called Dangote Foods to reflect the addition of the Rice and Salt companies. Transactions like this are lengthy affairs that involve courts, regulators, and government agencies and last up to 3-6 months. The process might be accelerated because certain legal exemptions on internal restructurings could mean the merger falls outside the Federal Competition & Consumer Protection Commission's (FCCPC) purview.

As part of the deal process, A 60-80 page scheme of merger document prepared by Dangote's investment bankers will be presented to shareholders for consideration. The document will provide the necessary information for investors to make an informed decision, and it will contain the following:

Timeline for Key Events

Letters from the Chairmen of each company's board of directors

Explanatory statements by the financial advisers

Valuation based on:

Historical Market Price Analysis;

Net Asset Value

Comparable Trading Multiples Analysis;

Comparable Precedent Transaction Multiples Analysis; and

Discounted Cash Flow Analysis.

Pro-forma financials of the surviving entity

With the scheme of merger documents, it's easier to know critical variables like the privately-held Dangote Rice's value and the surviving entity's listing price.

Yet, investors have bought heavily into the involved companies, presumably based on only the announcement of partial merger terms and publicly available financial information.

The scheme consideration below shows that Dangote Foods will comprise the three companies in the ratio of 70%:14%:16% (DSR:NASCON:DRL).

Investors with 100,000 units of NASCON will receive 91,667 shares of Dangote Sugar. In comparison, the shareholders of Dangote Rice (mostly Aliko Dangote himself) will receive 1,400,000 shares of Dangote Sugar for every 100,000 units in Dangote Rice.

Scheme Consideration

Eleven (11) ordinary shares of 50 Kobo each in DSR, credited as fully paid-up shares, for every Twelve (12) NASCON shares of 50 Kobo each, which totals 2,428,651,847 new ordinary shares of DSR; and

Fourteen (14) ordinary shares of 50 Kobo each in DSR, credited as fully paid-up shares, for every One (1) ordinary shares of N1.00 Kobo each in DRL share, which totals 2,775,792,508 new ordinary shares of Dangote Sugar Refinery.

The issuance of new shares could dilute existing shareholders in Dangote Sugar, and at current prices, the exchange ratios appear less favorable for investors in NASCON. The listing price of the surviving entity is an indispensable input needed to make judgments about whether or not the offer will sufficiently compensate investors.

Price is What You Pay, Value is What You Get.

As of March 2023, Dangote Sugar was trading at 17 Naira per share, a market capitalization of N205bn.

At that time, the business had just released it’s annual report where it posted N400bn in revenues, N80bn in levered free cash flows, and a 142% rise in net profits to N54bn in 2022. Its return on equity averaged 23% over the last five years. Their business model gives them strong pricing power as 95% of their sales are to distributors or manufacturers of confectioneries. This model gave them the ability to increase their average selling price by 33% while also growing unit volumes by double digits.

I did a discounted cash flow analysis using simple historical averages of the company’s following metrics:

Revenue growth

EBITDA margins

Capital Expenditures as % of revenues

Depreciation & amortization as a % of revenues.

I used a discount rate of 19%-20% and assumed that revenues in perpetuity would grow just below the historical nominal GDP growth rate of 13%.

With these assumptions, Dangote Sugar’s equity value is somewhere between N570bn-N815bn. At the market capitalization of N205bn, the company's shares were trading at a significant discount to even conservative estimates of its intrinsic value and should have been on every value investor's radar.

Prior to the merger announcement, the company published its June 2023 results where it reported a net loss of N30bn caused by the devaluation of the naira. The shares immediately dropped 10%. However, if you exclude the unusual expense, its normalized LTM earnings were over N7 per share. The company was effectively trading at 3.8x earnings at its price of N27 in June. If you apply its historical multiple of 7x, then it should have been trading at N50 per share.

A similar analysis of NASCON‘s equity value yields a fair value estimate of N130bn (N50/share) with a range of N110bn-N160bn.

Because 84% of the new entity will comprise the two publicly listed companies, we can make some assumptions about Dangote Rice using the exchange ratio to arrive at a reasonable guess for the intrinsic value of Dangote Foods.

If we assume the exchange ratios were calculated based on each company's intrinsic value, Dangote Rice's implied equity value is somewhere between N125 and N180 billion. Summing up the numbers for each company means that Dangote Foods' intrinsic value could be between N815bn - N1.16trn or N48-N67 per share.

As we have already seen, however, a company's intrinsic value can differ significantly from its stock price.

Security prices are often determined by events and how investors react to those events, which is primarily a function of how the events stack up against investors' expectations.

The main event in this case will be the listing price of Dangote Foods after the technical suspension that will be placed on it towards the end of the merger process and how it stacks up to the market’s expectations

We could estimate pro-forma financial statements for the new entity and then conduct a relative valuation to get a sense of what multiples the market could apply, but the lack of critical information will not make the results meaningful.

There are also investment bankers working late somewhere on the island who have been paid lots of money to do this -- so I would rather wait for their explanatory statements.

I enjoyed this fascinating book about Nigeria’s pre-colonial history. It gave me deeper understanding of the nature of political power in Nigeria through it’s explanation of succession practices in the various pre-colonial empires that existed at the time.

Nigeria exports about 5% of GDP to China every year, so a potential slowdown in China could have a serious effect on the economy and markets.

Important Disclaimers

Markets Markets Markets is not operated by a broker, a dealer, or a registered investment adviser. Posts on Markets Markets Markets are not intended to constitute, and should not be construed as an offering of advisory services or an offer to sell, or solicitation of any offer to purchase, any securities or other investments.

None of the posts on Markets Markets Markets contain the information that an investor should consider or evaluate to make a potential investment and are intended only to provide limited information to members of the public who have a legitimate interest in that information for reasons unrelated to making investments. Any references to specific securities, portfolio companies or investments are solely for informational purposes. If you would like investment, accounting, tax or legal advice, you should consult with your own advisors with respect to your individual circumstances and needs.

Posts on Markets Markets Markets are not aimed at the residents of any particular country and are not directed at, or intended for distribution to, or use by, any person in any jurisdiction or country where such use or distribution would be contrary to any local law or regulation or would subject the publication to any registration or licensing requirement in such jurisdiction. Those who choose to access Markets Markets Markets posts do so on their own initiative and are responsible for establishing the legality, usability and correctness of any information or materials under any or all jurisdictions and the compliance of that information or material with local laws, if and to the extent local laws are applicable.