Risky Business: Mispricings in the Nigerian Capital Markets

In order to understand what I see as abnormal conditions in the Nigerian capital market, it is important to define and understand risk and its relationship to returns. I am sure the more seasoned professionals reading this are not too keen on a lesson in what most would consider to be basic finance; however, I think it is important to return to first principles to gain meaningful insights on these peculiar market conditions. Risk is the most important factor in investing and this will also outline much of the risk management framework I use when investing for myself or through Panorama. I think this post will also be useful for anyone doing valuations on African securities who is struggling to arrive at a reasonable cost of equity to determine a discount rate.

Modern capital market theory is a good starting point in building a framework for understanding risk, with some important caveats. Capital Market theory defines risk as volatility because volatility indicates the uncertainty or unreliability of an investment. Volatility, especially in the context of standard deviation or variance, provides objective numbers with historical values that can be used for calculations and financial models, and truly, there is no substitute for these purposes.

As Howard Marks put it, volatility certainly can be a symptom or an indicator of riskiness, or even a specific form of risk. However, it is not the risk most investors are concerned about. Investors don’t seek higher returns because the price of an asset may show big fluctuations, rather, they seek higher returns primarily because they are afraid of losing money [1]. A downward fluctuation does not present an issue as long as the investor can hold on and come out the other side, but a permanent loss can never be undone. So, I will define risk, like many value investors have, as the likelihood of permanent capital loss.

Where everyone can agree with academicians is that risk is a bad thing. Much of modern economic and financial theory is based on an underlying assumption that people are naturally risk-averse and, ceteris paribus, they would rather take less risk than more risk. Given this assumption, investors must be enticed with the prospect of higher returns in order to take incremental risks.

If, for example, a group of rational investors are given the choice between a government security that promises 7% per year (with the knowledge that governments can simply print money to pay them back so will not default) and a small startup stock likely to generate the same return, investors will rush to buy the government security (thereby increasing its price and reducing its return) while the latter will be dumped, driving down its price and increasing its potential return. This process is called equilibration and it is the mechanism by which markets adjust relative prices to make returns proportional to risk.

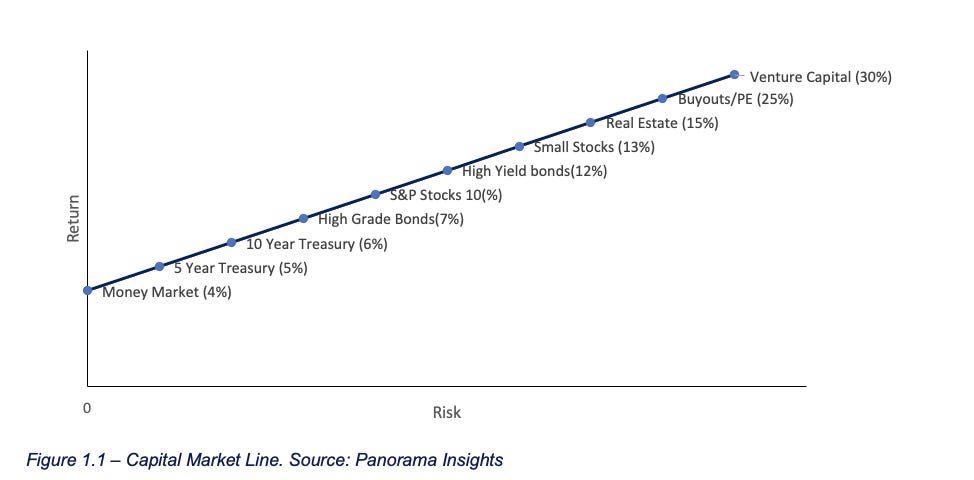

Defining and understanding this process is quite important because while the positive relationship between risk and return is well understood by the average person, that relationship, without an understanding of the mechanism that drives it, can breed fallacies. One such misconception that is particularly common in bull markets is “If you want to make more money, you must take more risk because riskier investments provide higher returns”. reality is that riskier investments must offer the prospect of higher returns in order to attract capital. If riskier investments consistently produced higher returns, they simply would not be riskier. This misplaced reliance on the benefits of risk-bearing has led many investors to some very unpleasant surprises. The process of equilibration and the subsequent positive relationship between risk and return culminates in a familiar capital market line illustrated in Figure 1.1 below.

The capital market line illustrates the positive relationship between risk and return; investments that seem riskier must appear likely to deliver higher returns; otherwise people will not make them. In a rational market, the price of a risky asset will be set low enough that the reward for holding them appears to compensate for the risk sufficiently.

This brings us to the unique situation in the Nigerian capital markets and what I view as a breakdown in the risk-return relationship.

As with many developing countries, inflation remains relatively high and the risks that investors are primarily concerned with avoiding are related to the erosion of their purchasing power. A secondary issue, yet equally important to investors, is protection from currency devaluations in Nigeria. In reality, these two issues are effectively the same due to relative purchasing power parity.

The law of one price dictates that an identical asset or commodity will have the same price globally, regardless of location (assuming a frictionless market). This exists because differences between asset prices in different locations would eventually be eliminated as market equilibrium forces align the asset prices due to the arbitrage opportunity. Exchange rates are designed such that the rate of exchange is equal to the ratio of price levels between two countries. As inflation erodes purchasing power at different rates in different countries, the price levels change and so do the exchange rates.

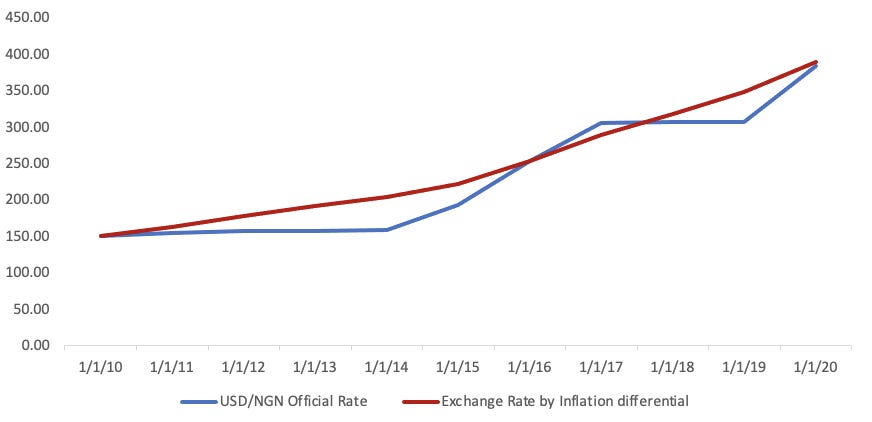

As inflation in Nigeria is generally higher than the United States, the currency is devalued to maintain parity. This erosion in purchasing power is fairly constant but appears lumpy due to the fixed exchange rate system operated by the Central Bank of Nigeria. The difference in the rate of inflation between the two countries has averaged around 10% per year and changes in the actual exchange rate have roughly matched that over time. This is illustrated below in Figure 1.2 which compares the official exchange rate to the nominal exchange rate calculated using the yearly inflation differential between the US and Nigeria using 2010 as the base year.

In 2010, N1,000,000 was worth approximately $6600 and by the start of the next decade, the same N1,000,000 would only be able to purchase $2500 worth of goods. In other words, for investors to have avoided an erosion of purchasing power and earned a zero US dollar return, their N1,000,000 must have grown to N2,600,000 over 10 years representing a CAGR of 9.99%.

Importantly, Inflation in Nigeria has averaged around 11.9% annually over the last 10 years. In an attempt to beat inflation and earn a positive real return, investors also protect themselves from the risk of devaluation because movements in the exchange rate are correlated with, if not caused by, the difference in inflation between the US and Nigeria as illustrated in Figure 1.2.

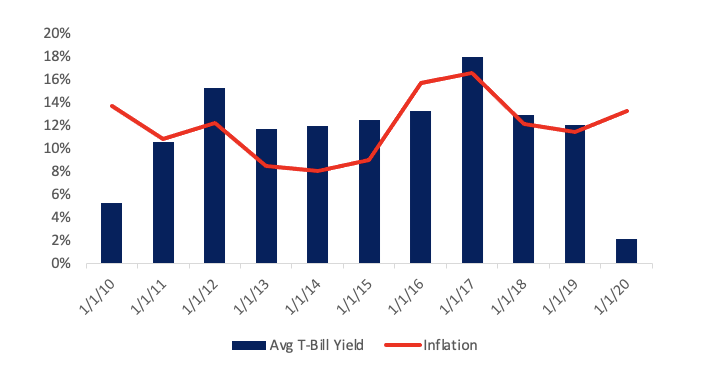

Average yields on naira securities such as treasury bills and FGN bonds over the last decade show that investors have demanded an average return that closely matches or beats inflation as the risk-free rate. This is illustrated below in Figure 1.3 tracking the average annual true yield on treasury bills with the rates of inflation. Treasury bills were selected as the proxy for the risk-free rate because they lack reinvestment risk due to being zero-coupon securities, and their yields at auction more closely represent investors' demands.

Given the high rates of inflation and the subsequently high rates of return on risk-free securities, we would expect the capital market line for Nigeria to be shifted upwards but to maintain the same positive relationship between risk and return whereby investors are compensated for bearing incremental risks with incremental returns. Moving up the risk curve to equities, we should expect that equities will offer a significant return over the risk-free rate, otherwise investors would not allocate capital towards them. Yet over the course of the last decade, fixed income and even riskless securities have outperformed the equities market and quite significantly in certain instances.

The extra returns demanded (or that should be demanded) by investors in order to invest in stocks is the equity risk premium. It is fairly common practice to estimate the equity risk premium by analyzing historical data on the market returns of equities compared to the risk-free rate. Given the fact that the returns on risk-free securities exceeded the return on equities in Nigeria over the last ten years, an analysis of historical risk premiums would not yield much insight.

Even if the equity risk premium were not negative, the results generated from historical premiums tend to be overly sensitive to the amount of data used and a 10-year time period would result in standard errors in excess of 6%. The choice of Treasury bills or Government Bonds as the riskless security and whether an arithmetic or geometric average is applied also cause large variations in estimating the equity risk premium.

Due to the challenges associated with historical premiums, we can once again turn to the capital asset pricing model to estimate the equity risk premium. I lean particularly on the work of Aswath Damodaran, a renowned professor of finance at the Stern School of Business at New York University. His estimation method uses the difference in Credit Default Swap (CDS) spreads between the United States and the target country to arrive at a country risk premium that is added to the implied equity risk premium of the S&P500 to come at a total equity risk premium [1]. Applying this method to Nigeria yields an estimated equity risk premium of 10.05%.

Having estimated the equity risk premium above, we can calculate the cost of equity using the capital asset pricing model:

Cost of Equity = Risk-Free Rate + Beta x Equity Risk Premium

For the risk-free rate, we start with the interest rates on long-term FGN bonds but subtract the country default spreads because investors perceive default risk in the Nigerian Government. We arrive at a ratings-based default spread of 4.82% based on Nigeria’s B2 rating by Moody’s[2]. Using these inputs results in a cost of equity of 19.18%, which is how much investors should demand from equities to compensate for the risk.

Naturally, the question that follows is why haven’t Nigerian equities returned enough? The answer seems deceptively simple; the listed companies have a return on equity far below this, so most businesses just are not profitable enough to compensate for the risk of doing business in Nigeria. There are, however, companies that have returned more than the cost of equity (and quite consistently for over a decade). Yet, their total shareholder returns do not meet this benchmark we arrived at in the preceding paragraph. For a company to return, say, 30% on its equity, year after year but not receive a commensurate 30% total shareholder return implies that the market constantly de-rates these companies and is willing to pay less for each Naira of earnings. Naturally, this has led to Nigerian stocks being much cheaper relative to their emerging market peers and relative to the Nigerian market’s own historical valuations.

I didn’t intend for this post to explore the potential reasons why this is the case but rather to prove that there is a breakdown in the risk-return relationship, and it is most likely because our companies are being priced exceptionally harshly. I will also say that investors are people, and people don’t always act rationally. I don’t think it’s surprising that investors are pessimistic when the country has gone through one of the worst economic stretches in its history. However, does it make sense to price its stocks as though the country will never recover? I think not.

[1] Marks, H. (2011). The most important thing. Columbia University Press.

[2] Damodaran, A. (2021). Country risk: Determinants, Measures and implications — the 2021 edition. SSRN Electronic Journal