Hyperinflation.ng

How far along are we on our journey from Lagos to Caracas?

No one knows the rate of inflation in Nigeria.

Everyone feels intuitively that the 18-19% number by NBS is nothing but a fantasy. And they’re right. NBS has not updated its basket of goods or their weighting since 2009, which means that they are tracking changes in the price of products that are probably not consumed by the average Nigerian. This economic think-tank estimates the inflation rate to be more like 45%. That seems like a realistic number, but I know personally my basket of goods is inflating at a rate higher than that, and anyone that consumes a lot of diesel is probably in the same boat (but certainly won’t represent average Nigerians).

I think a lot of Nigerians have nursed the thought in the back of their heads that we could be headed towards hyperinflation but with no way of actually knowing. Most people understand what hyperinflation is and can probably tell you that it’s usually caused by printing too much money but without a deeper understanding of how one plays out.

Hyperinflations are almost always the result of prolonged boneheaded policies by governments and central banks. Virtually every hyperinflation has been caused by deficit monetization AKA printing money to pay for excessive government spending. If you have even heard of the words “ways and means” before, you are probably getting sick to your stomach right about now.

Now, every hyperinflation was caused by printing too much money, but not every case of excessive money printing causes hyperinflation. So what causes some cases to spiral and others not to?

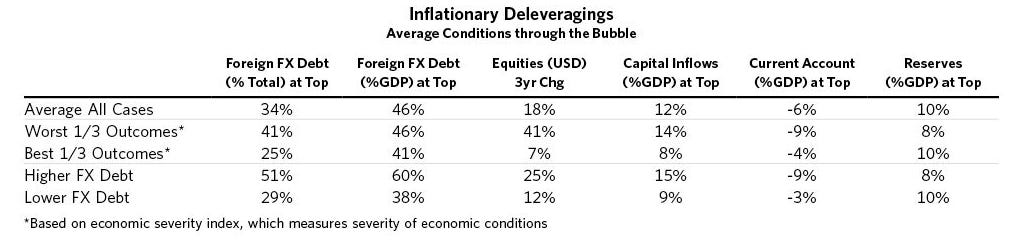

Luckily for me; Ray Dalio, the founder of the largest hedge fund in the world, spent a lot of time and effort studying the 27 most severe cases of inflationary deleveragings to map out the archetypal case. If you want a broader understanding of debt crises you can read his research for free here. I’m going to use some of the key metrics he uncovered to map out how severe our inflationary depression has been, and how much we share in common with the cases that spiral into hyperinflations.

Generally speaking, the greater the degree to which these things exist, the greater the degree of the inflationary depression. Nigeria literally ticks every last one of those boxes and surprise surprise we have had a severe inflationary depression for much of the last decade. An “inflationary depression” is just as it sounds; a period of economic depression characterized by high inflation rates and the short story is that they are caused by countries spending more foreign exchange than earn.

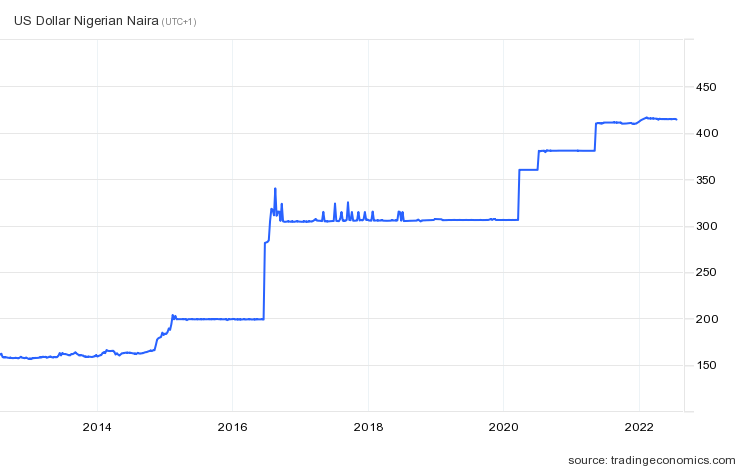

Like many of the other cases analyzed by Bridgewater, ours started with a fall in income due to reduced exports and a concurrent decline in capital flows coming into the country. When the oil price crashed circa 2014, the value of our exports dropped meaning we started earning less FX than we were spending, creating downward pressure on the naira and a gap that has to be closed somehow.

I will admit that it puts both politicians and central bankers in a difficult position. They can choose to either:

let the currency depreciate

increase interest rates or

spend down foreign reserves.

These choices all result in bankers getting less economic growth per unit of inflation. Realistically, raising interest rates to fill a balance of payments gap isn’t an option. If the currency is expected to decline 5% in a year, then interest rates would have to go up by 5% to keep it at the same price. So even a very small currency decline means a huge interest rate premium. Increasing interest rates by 5% in a year is enough to crash many economies. Now imagine a 5% currency decline per month, it would mean interest rates increasing by 80% per year, and then remember that the naira depreciated 10% just last week on the parallel market.

This leaves bankers with the choice of either spending down reserves or allowing the currency to depreciate. Most central banks choose to defend their currency and Nigeria is no different. Due to ideology* we also got additional measures like capital controls and import restrictions all to close the FX gap. While Central bankers are happy to spend reserves to defend the currency, most sensible ones will not risk running out of savings, so they will still allow a managed depreciation of the currency which is what we have seen for the IEFX rate in Nigeria.

In all inflationary depressions, currency depreciation translates to more expensive imports, much of which is passed on to consumers, resulting in a sharp rise in inflation. The way policymakers manage the currency decline during these depressions greatly affects how much inflation there is and how it plays out.

A gradual and persistent currency decline causes the market to expect continued currency depreciation, which can encourage people to speculate and send their money abroad, widening the balance of payments gap. A continual devaluation also makes inflation more persistent, feeding an inflation psychology. The CBN in this 2018 study found that “Expected inflation constitutes the most significant predictors of inflation in Nigeria.” Talk about inflation psychology. We’ll come back to why this is particularly bad.

Counterintuitively, it is better to have a large one-off devaluation. This only works when the currency is devalued enough that there are both willing buyers and sellers and there is a positive total return for holding Naira. If the currency falls enough very sharply, people won’t expect more devaluation. The 2016 recession followed the archetypal inflationary depression to a tee. Despite the very large devaluation, other poor policy choices have meant that we haven’t had the sort of recovery you would expect.

Perhaps naively, I always thought there was no theory behind Meffynomics and everything was just being done Jaga Jaga. The reality was shocking and worse. Buhari, and by extension Meffy, believe in and practice import substitution industrialization (ISI). It’s why after escaping a long-term depression by the hem of our garments, the government decided to shut its border during a trade surplus to “stop smuggling” and “boost local production”. Make no mistake; the government budget deficits and current account deficits are features of Import Substitution Industrialization which is part and parcel of the African socialism that their generation of politicians came up on.

The Spiral from a More Transitory Inflationary Depression to Hyperinflation

The research is very clear. The most important characteristic of cases that spiral into hyperinflations is that policymakers don’t close the imbalance between external income, external spending, and debt service, and keep funding external spending over sustained periods by printing lots of money. As of June 2022, the CBN has printed N19 trillion (almost $50bn) to finance Buhari’s government deficits over the last 7 years via the Ways and Means advance.

When continual currency declines lead to persistent inflation, it can become self-reinforcing in a way that nurtures inflation psychology and changes investor behavior. With each successive currency decline, savers and investors, who were burned before, now move to protect their purchasing power. They are quicker to short cash and buy foreign and physical assets. You see this today where many people without USD expenses convert their entire salaries to dollars when possible. The result is currency devaluation that no longer stimulates growth.

Understandably, as inflation gets worse, depositors want to be able to spend their money as fast as possible and put them into real assets. As it continues to worsen, people would be happy to get loans to short cash because it is so profitable to do so. Frighteningly, it seems people are becoming confident enough to take out bank loans to buy dollars at the parallel market rate because the interest rates on the loans are less than the amount of depreciation. Something that I think gets swept under the rug is that as the currency declines, the burden of the debt increases in local currency. Whatever ‘low’ debt to GDP numbers we have can be nearly instantly ramped up by severe depreciation.

It’s easy to see how these forces can create a feedback mechanism that causes inflation and currency declines to escalate until people completely lose faith in the currency and people aren’t willing to hold more than a few days of cash at once. I’m not saying we are destined for hyperinflation especially because some of our metrics are slightly better than the averages in the image above - but of course, averages are misleading and it also assumes that Nigeria’s data is accurate.

Really enjoyed reading this. It lays out Nigeria's Macroeconomic outlook very succinctly. Fortunately(or not), a year later this piece is still relevant.